Let’s talk money, Covid-19 style.

The US GDP dropped by 4.8% in the first quarter of 2020, bringing its decade long economic expansion to a screeching halt. White House economists estimate another drop of 20% – 30% in the current quarter.

To me, this looks economically like the end of WWII and politically like the 1929 market crash. The economic downturn at the end of WWII was characterized by an upheaval in the labor market as soldiers returned home accompanied by worldwide political alignment to repair the system. The 1929 market crash, on the other hand, was characterized by an upheaval in the financial market accompanied by worldwide political thrashing largely over nationalistic tariffs. The Trump downturn is characterized by an upheaval in the labor market as people cloister themselves from Covid-19 accompanied by worldwide political thrashing largely over nationalistic tariffs.

It boils down to this: Trump played a strong hand poorly. He made risky moves in trade and fiscal stimulus which, if they were ever to succeed, could succeed only in the absence of exogenous events disrupting the economy. As Trump ratcheted up tariffs and spiked a US$1 trillion deficit with tax cuts for corporations and oligarchs, the world delivered a Spanish flu magnitude pandemic.

If you’d told me in 2017 that Trump’s policies would leave the country in economic shambles with people dying, my only question would have been whether it was a nuke from North Korea or a dirty bomb from a terrorist. Only a few people like Bill Gates had their eyes on a pandemic as Trump dismantled America’s response team and healthcare system.

I don’t pin the economic downturn on Trump. Even with less risky economic policies, any administration would have experienced a Covid-19 economic shock just as the rest of the world has. The American Covid-19 response, though, lies squarely on Trump’s drooping shoulders. He already has taken the best options off the table. He has reduced the chances of an American V-shaped recovery because his risky policies give the US fewer fiscal stimulus options and fewer international friends to coordinate the worldwide changes now required.

The looming economic tragedy in the US goes hand in hand with Trump’s deadly public health response to Covid-19. With a steadier hand, the US would not have paid such a high price for Covid-19 in dollars and souls.

Spain today says it expects an asymmetric V-shaped recovery (which looks kind of like a square root “√” shape rather than a “V” shape).

Spain and most of Europe will see less unemployment than the US, largely because companies are not allowed to fire employees. This may seem strange to Americans who haven’t worked internationally, but European labor law gives workers better footing in the economic dynamic between labor, management, and ownership. This labor preference comes with trade offs, of course. European companies try to hire fewer people because it’s harder to fire them.

In the Covid-19 economic meltdown, which is essentially a massive labor force discontinuity, theses differences in labor law are leading to vastly different labor market outcomes. In the US, employees are fired. That means that owners and oligarchs bear the cost of supporting labor by paying taxes so the government can provide unemployment benefits. Since Trump has cut taxes, owners and oligarchs aren’t paying anything. Instead, the US is borrowing like crazy to pay unemployment benefits. In Europe, labor keeps its job. That means that owners and oligarchs bear the cost directly of supporting labor with subsidies from the government.

My unemployed US friends are figuring out how to navigate overburdened state unemployment systems. Their benefits will be limited by how much the US government can borrow. My employed Spanish friends are figuring out how to live on reduced salaries. Their salaries will be limited by government subsidies to business and the ability of business to remain solvent. In the US, unemployment is largely paid by government, while in Europe employment is paid by the owners and oligarchs who are subsidized by government. The US risks its ability to borrow more money, the Europeans risk weaker businesses going belly up. As the economy revives, Europeans will go back to work faster because they already have jobs.

Parenthetically, small US businesses are walking a tightrope. Not surprisingly, more than half of US small cap CFOs are slow walking vendor payments. That may be, in part, because the US Payroll Protection Program is struggling to get massive amounts of stimulus to the right parties. My friend Todd talks about the inadequacy of channeling PPP through banks. If the Trump administration ever gets PPP working, it may provide essentially the same job subsidies to small US businesses that European countries are providing to all businesses.

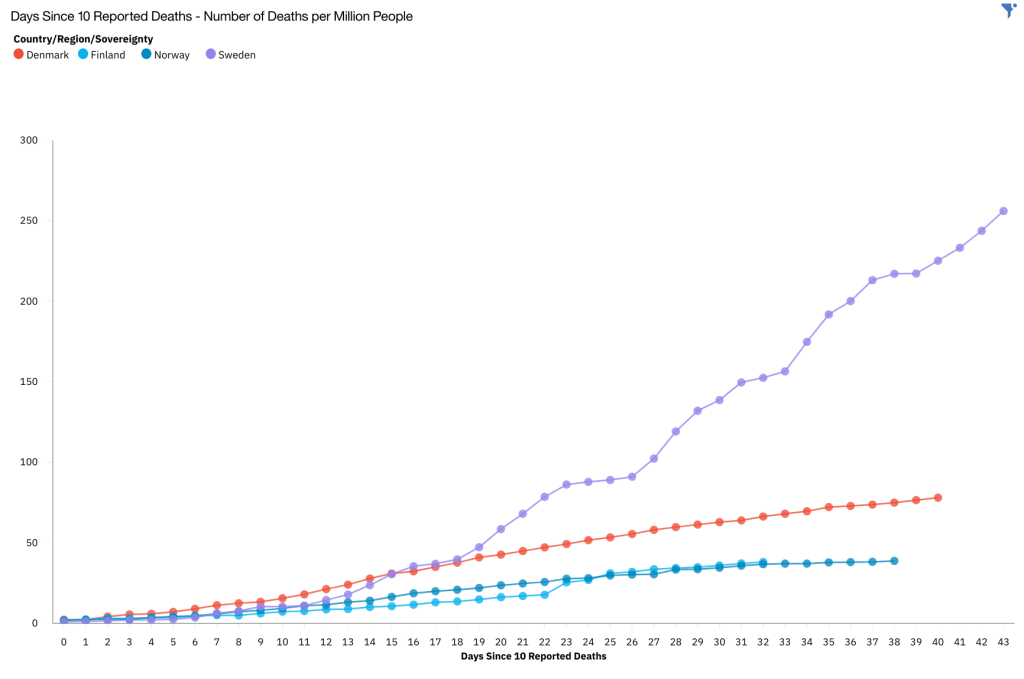

Speaking of Europe, let’s talk about Sweden. I’m currently of the opinion that Sweden’s PR Department is doing a better job than its Public Health Department.

The anti-lockdown contingent is promoting Sweden’s lockdown-lite as a huge success at saving its economy while providing adequate safety. First, we don’t really know how Sweden’s economy is doing compared to its Scandinavian neighbors or Europe. Second, compared to neighboring countries with strict lockdowns, I have to say, looking at the chart above, that Sweden’s lockdown-lite is kind of a disaster. While Norway, Denmark, and Finland have flattened their Covid-19 mortality with strict lockdowns, Finland clearly has not got its infection rate R below one yet. So, if 5x – 6x higher mortality is acceptable for maybe saving a country’s economy (we don’t know yet), well, Sweden is your prime example.

Parenthetically, the anti-lockdown movement is focused on IFR, claiming that Covid-19 IFRs are low, about the same as the flu. There are two problems with their argument. One is that it’s hard to measure IFRs and estimated IFRs have a wide range. We don’t understand yet whether the wide range is due to testing methodology, adjustment methodology, different Covid-19 strains, different population characteristics (e.g., BCG vaccinations), or some other factor. The other problem is that we’re probably using the wrong IFR for the flu. The CDC estimates for flu deaths are estimates, not counted deaths. If you compare counted flu deaths to counted Covid-19 deaths, it looks like Covid-19 is 10x – 45x more deadly than the flu.

Next door to Sweden, Russia is running off the rails. Gail sent me a couple of good pieces about a part of the world that has kept its Covid-19 problems under wraps. I’ll have more on Russia in a later post, but on the economic front, it’s hard to tell which is harder on the Russian economy right now, oil prices or Covid-19. With oil prices as low as they are now, Putin is hesitant to spend any of Russia’s his US$150B sovereign wealth fund. You read that right. US$150B. While the US is borrowing trillions of dollars to paper over Covid-19 problems, Putin has a fraction of that in his reserve fund and no oil income. Good luck, Vlad!

Vlad shouldn’t feel to blad about things. Even drug dealers are having money problems. Wholesale meth prices have doubled as supplies dwindle and cartels can’t move cash out of the US. The DEA seized more than US$1 million in each of three recent Los Angeles raids.

With storefronts closed, supply chains in disarray and the global economy in peril, these complex schemes are hobbled and cash is backing up in Los Angeles …

Los Angeles Times, “Dirty money piling up in L.A. as coronavirus cripples international money laundering,” 30 April 2020

Cartels rely on non-essential businesses in LA to accept US dollars for goods, and then ship goods to Mexico to be re-sold. Those businesses are largely closed during the Covid-19 pandemic. And you know that when the cartels are having money problems, it’s a really bad economy.

Speaking of cartels, there’s the Trump Organization whose cash generating properties have been closed by the Covid-19 pandemic. Yahoo sent reporters to suss out the president’s Washington, DC property, Trump International Hotel. They found lots of room to distance socially.

“This is a market segment that is downplaying the risk of COVID-19. If you’re going to tie yourself to the president, and you think it’s important enough to go to the hotel, you’re not going to let fear of pandemic keep you away.”

Zach Everson, author of 1100 Pennsylvania newsletter, on Trump International Hotel’s post-Covid-19 prospects.

When the US capitol relaxes its Covid-19 restrictions, the President’s supporters will be the first to return to Trump International, happily sharing their Covid-19 stories and their Covid-19.

Meanwhile, Trump will continue blaming China for Covid-19. Never mind US intelligence says China didn’t release Covid-19 from one of its labs. Trump can’t pay off his Chinese loans, so he needs something to negotiate with. It’s important to the rest of us to find out the actual origin of Covid-19 so we can prevent another outbreak. Money is all that matters to Trump, especially other people’s money in his pockets.

That leaves me with no time to talk about one of the most interesting financial articles Brad passed my way recently. But you can read it here. This is how weird things are getting in the Covid-19 depression.

Last of all today, a shout out to my friend Ken on his 70th solar rotation. Ken’s birthday is a nice reminder that life keeps going while we’re sheltering in place. Keep stretching, Ken!

One thought on “1 May 2020 – Friday – #47”

Comments are closed.